Your local mortgage brokers & home loan expert in Ringwood, Croydon & Lilydale

When it comes to a big decision like your home loan, having the right team on your side - a team like Mortgage Choice Ringwood - can make a big difference. Our free home loan service will save you hours of research and paperwork, and help make your next step a great one.

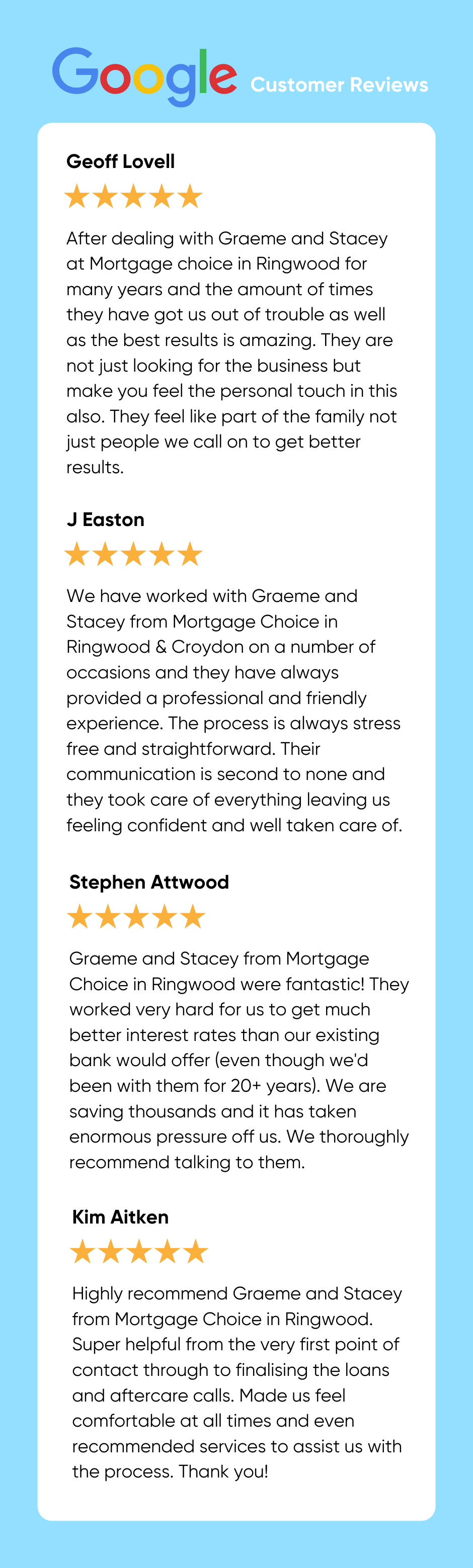

Ringwood

5.0

(94+ total reviews)

Aggregated from:

![]()

![]()

![]()

![]()

![]()

- Call Us

- Office - 03 9876 8455

- Fax - 03 9876 8488

- Open Hours

-

Monday - Friday: 9:00am - 5:00pm

After hours by appointment

Address

Suite 1, 1st Floor, 164 Maroondah Hwy RINGWOOD, VIC 3134

Latest home loan interest rates

Starting from

%*

p.a.

Comparison rate

%#

p.a.

Expert advice for the next step in your finances

With a big step like choosing the right home loan, you'll need a team of experts on your side - like our team at Mortgage Choice in Ringwood. We know what's available & can get you the right loan with a great rate & features.

How we can help with your hmoe loan

You might already know just how many loan options are available in the market right now. If you have information overload or are just short on time, our Mortgage Broker Ringwood team will do the work for you. We have over 30 lenders on our panel and know where to look to find you a great one.

- We sit down with you to figure out your budget & goals. The Mortgage Broker Ringwood team will figure out how much you can borrow & what your repayments might be.

- We do all the research and shopping around for you, searching through thousands of home loans to find you a small selection of great loans to suit. We'll talk you through the pros and cons of each.

- We explain everything in a way so that you fully understand of each home loan product and can confidently make an informed decision. With our guidance, you make the final choice on what product you think will suit best.

- We'll complete the paperwork on your behalf and keep you updated on how the loan is progressing all the way through to settlement.

All at no cost to you

As Mortgage Brokers in Australia, we offer our home loan service at no cost to our customers! It means that everyone, no matter what you're looking to purchase, has access to expert home loan advice that is separate from the banks and in your best interest.

We'll help you take the next big step

Our Mortgage Broker Ringwood team have years of experience in finding the right home loan for our customers. With the right rate and right features, we will structure your home loan to work for you in the long run.

Our team of brokers are mobile and able to come by at a time & place that suits you. We also have a conveniently located office at 164 Maroondah Highway in Ringwood.

Call Mortgage Choice in Ringwood on 03 9876 8455 to chat about your next steps in property. We're excited to get started!

Call: 03 9876 8455 Request a call back

The Mortgage Broker Ringwood team service the areas of: Wattle Glen, Hurstbridge, Strathewen, Donvale, Warrandyte, Park Orchards, Chirnside Park, Ringwood, Ringwood North, Warranwood, Heathmont, Ringwood East, Croydon, Croydon Hills, Croydon North, Croydon South, Kilsyth, Kilsyth South, Mooroolbark, Seville, Wandin East, Wandin North, Lilydale, St Andrews, Tarrawarra, Yarra Glen & across Victoria.

The right home loan for your needs

Our mission is to find the right home loan for your individual needs and to always have your best interests at heart. Plain and simple. Which is why we have such a wide range of lenders to choose from. We can search through hundreds of products to find something tailored to your situation. ~

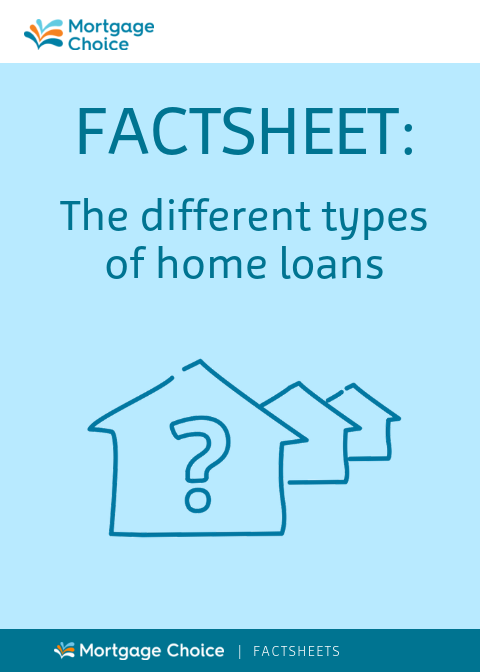

Factsheet: The different home loan types | Mortgage Broker Croydon

Choosing the right home loan is important, and can be a tricky decision if you don't understand what makes each type different! Our team at Mortgage Choice in Ringwood & Croydon can help you understand more about the lender & home loan type that will suit you and your budget. In meantime, download our free factsheet on the different home loan types along with pros & cons of each.

Help me calculate

Latest news & tips