Asset finance

Everything you need to know about asset finance

July 23, 2024

Refinancing refers to the process of paying out your current home loan by taking out a new loan, either with your existing lender or through a different lender.

What's involved in refinancing a home loan?

Replacing your current home loan with a new one

Receiving additional or better features

Exit fees and borrowing costs to consider

Offering savings on interest

Our free home loan health check compares thousands of options with your current loan to see if you could save.

Plus, you could get up to $2,000 cashback^^ if you refinance with selected lenders and meet their eligibility criteria.

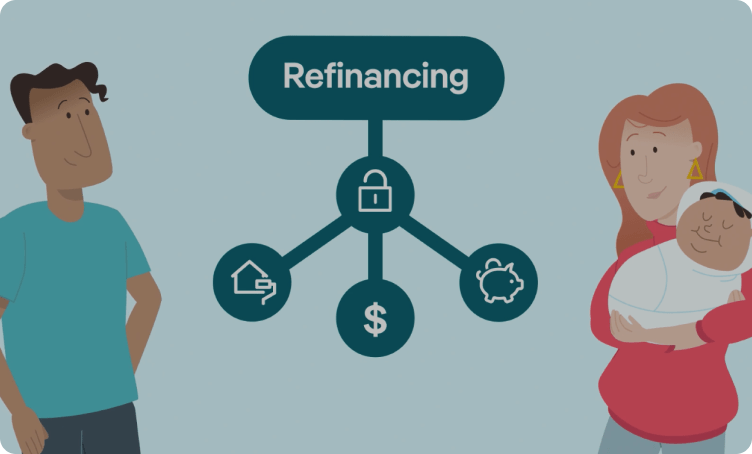

If you’ve been paying off your home loan for a number of years, you may have built up equity that is available to access. Home equity is the difference between your current property value and your remaining debt. In order to understand how much equity you have, you’ll need to get a property valuation, and then you’ll be able to access your available equity by refinancing your loan.

Refinancing is often a strategy used to free up the equity you have in your current home in order to fund purchases or lifestyle goals. You can refinance your home loan and use your equity for various reasons, including home improvements, car loans, a holiday and even to purchase an investment property.

There can be some fantastic benefits in refinancing your home loan - just make sure you also weigh up the different expenses outlined below that can be involved in the transfer to make sure it’s the right choice for you.

Why refinancing a home loan can be a sensible step

If you’re keen to secure a better interest rate or enjoy more loan features, refinancing your home loan can be the solution. Refinancing is also an opportunity to get control of debt or tap into any home equity you’ve built up.

The most popular reason home owners choose to refinance a home loan is to secure a lower interest rate and reduce their monthly repayments. However, refinancing can come with some costs, so it's essential to weigh up the savings of refinancing against the expense involved.

If you'd prefer the certainty of repayments will stay the same for a period of time, you may wish to switch to a fixed rate. Refinancing your home loan lets you do this. Or, you may decide you'd like to take advantage of a lower variable rate as you can accept the risk that rates may rise in future.

Your home is likely to be one of your most valuable assets, and by harnessing home equity you have the opportunity to build additional wealth or simply achieve personal goals. Find out more about accessing your home's equity.

Like many Australians you could have several debts – probably a home loan, a personal loan, and possibly even a credit card balance. Having multiple debts means juggling lots of different repayments.

Refinancing your home loan can provide an opportunity to streamline your debt, and potentially reduce the overall interest you're paying on multiple debts through the process of 'debt consolidation'. It means folding several high interest debts into one lower rate debt – which could be your home loan - and this may reduce your total monthly repayments.

However, it's important to note that debt consolidation can come with some downsides. It can turn a short term debt like a personal loan into a long term debt (your mortgage), and that means paying interest on the balance for a much longer period which could cost you more in the long run.

For debt consolidation to be truly cost effective, you need to commit to making additional repayments to pay off the enlarged loan as quickly as possible.

Making extra repayments at no additional cost to help pay off the loan sooner.

A break from repayments or reduced repayments to cover career changes or breaks e.g. maternity leave.

Having a savings or transaction account linked to your loan. The balance of the linked account is deducted from, or offset against, the balance of your loan when the monthly interest charge is calculated.

Enabling you to withdraw any additional repayments you have made on your loan. Handy if you need cash in an emergency.

Dividing your rate between fixed and variable components, or even making interest-only payments for a period.

The ability to take your loan with you when you move from one home to another without the expense and hassle of arranging a new loan.

Depending on your circumstances, not all of these will apply. It’s worth having a chat with a Mortgage Choice broker to explore the costs involved with your individual situation, and balance these with any potential cost savings of switching home loans.

Understand the costs to refinance

Although exit fees have been banned on new loans taken out after 1 July 2011, they could still apply to loans taken out before this date.

Worth knowing: Exit fees don't include break costs, which can be imposed if you bail out of a fixed rate loan before the fixed term expires. It’s worth speaking to your Mortgage Choice broker if you are thinking about refinancing a fixed rate mortgage.

When you refinance, your new lender may charge a range of upfront fees. However not all lenders charge these fees and some may be negotiable.

They may include:

You may be able to capitalise LMI (add it to the loan) though you need to be careful that this won't push your level of borrowings over the lender's preferred 'loan to valuation ratio' (LVR) - the amount you borrow as a percentage of your home's value.

Some states charge a tax on your mortgage which is known as stamp duty, which is calculated on the amount of the loan. If you increase the size of your loan when refinancing, stamp duty may be payable.

You may also need to pay a Mortgage Registration Fee which is imposed by the Land Titles Office (or equivalent) for registering your mortgage onto the title record for the property.

Credit criteria, conditions, fees and charges apply. Subject to suitability. The comparison rates in this table are based on a loan amount of $150,000 and a term of 25 years. Warning: This Comparison Rate applies only to the example or examples given. Different amounts and terms will result in different Comparison Rates. Costs such as redraw fees or early repayment fees, and costs savings such as fee waivers, are not included in the Comparison Rate but may influence the cost of the loan.

If you’re thinking about refinancing, this guide can help you learn more about the refinancing process, benefits and options available.

Asset finance

July 23, 2024

Property investment

July 09, 2024

Property investment

June 25, 2024

Property investment

June 11, 2024